The Federal Reserve may seem far removed from your daily life. But the decisions it makes ripple out to affect everything from your mortgage rate to your credit card bill to the cost of groceries. Right now, with inflation cooling but the economy showing signs of strain, the Fed is once again front and center. And so is its Chair, Jerome Powell, who is drawing criticism from President Trump and others who want him to drop interest rates faster.

So what exactly does the Fed do, and why should you care?

What Is the Fed?

The Federal Reserve, often called “the Fed,” is the central bank of the United States. It was created by Congress in 1913 to help ensure the stability of the nation’s financial system. While its leadership is appointed by the President and confirmed by the Senate, the Fed operates independently from day-to-day politics.

Its job is to promote two key goals: maximum employment and stable prices. This is known as the Fed’s “dual mandate.”

RELATED: Why The Federal Reserve Matters

How It Tries to Meet That Mandate

To meet its goals, the Fed’s main tool is setting short-term interest rates, specifically, the federal funds rate. When inflation is too high, the Fed raises rates to make borrowing more expensive. That slows down spending and brings prices back under control. When the economy is too slow and unemployment is high, it lowers rates to encourage borrowing and investment.

The Fed also uses other tools, like buying and selling government bonds, to influence long-term interest rates and the flow of money through the financial system.

The Federal Reserve has adjusted interest rates 18 times in the last five years, dating back to the early days of the pandemic when rates were dramatically slashed to try and keep the economy afloat.

How Fed Policy Affects Your Wallet

The most visible effect of the Fed’s actions is on borrowing costs:

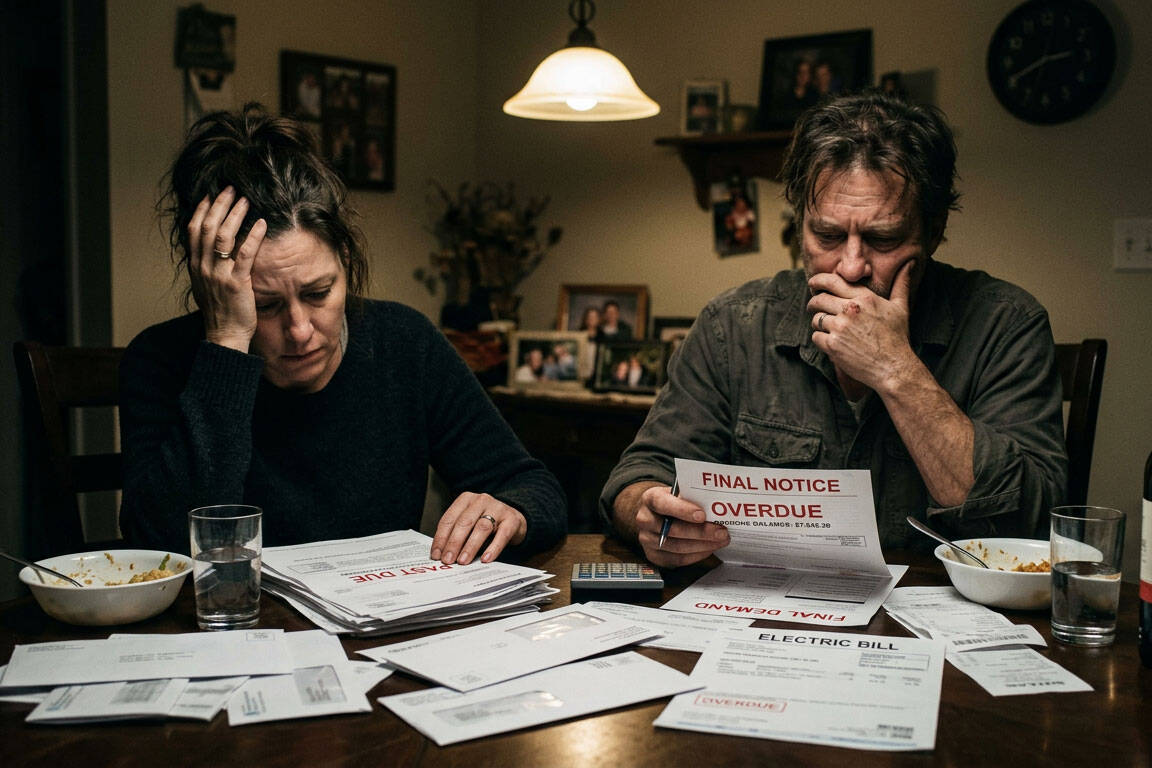

- Credit Cards and Loans: Higher Fed rates lead to higher APRs on credit cards, car loans, and personal loans. If you carry a balance, you are paying more in interest.

- Jobs: If the Fed raises rates too far or too fast, businesses may pull back on hiring, or even cut jobs, because borrowing and investment become more costly.

- Inflation: On the flip side, raising rates can help bring down inflation. That matters at the grocery store, the gas pump, and when you are budgeting for rent. In 1981, Fed Chair Paul Volcker hiked the federal funds rate to 20% to help tame the stagflation (a combination of slow economic growth and high inflation) crisis of the late 1970s. Inflation fell to 3.2% by 1983, though the economy entered a severe recession

Why Independence Matters

The Fed’s ability to act independently without needing approval from the President or Congress gives investors and consumer confidence that monetary policy is being made with the long-term health of the economy – not short-term political considerations – in mind. That independence allows it to make tough calls that might be unpopular in the short term but necessary for long-term stability.

The Bottom Line

Whether you are carrying credit card debt, or just trying to keep up with rising costs, the Fed’s decisions matter. Its work is sometimes arcane but it is essential.

Looking for the latest in your inbox? Sign up for emails from No Labels.

Related

Sam Zickar

Sam Zickar is Senior Writer at No Labels. He earned a degree in Modern History and International Relations from the University of St Andrews and previously worked in various writing and communications roles in Congress. He lives in the Washington, D.C. area and enjoys exercise and spending time in nature.